Lombard loans

When we described how DeFi banking works, we wrote that in oder for someone to obtain a loan, they need to lock in some collateral first. Fully collateralised loans, where both collateral and loan are ‘marked to market’ on an ongoing basis, are called lombard loans. Banks issue them all the time and when the loan value gets close to the collateral value, they issue a margin call, forcing their clients to sell their assets to cover the loan amount.

This usually happens when clients are suffering heavy losses and, if done in a disorderly fashion, this may force banks to use their open capital to cover the loan, leading to capital losses. The latest example of such a disorderly unravelling is the default of Archegos - a $20bn hedge fund, which couldn’t cover its positions and caused multi-billion losses across several major banks.

That’s why banks keep reserves - to mitigate situations when loans, supported by liquid volatile collateral, need to be repaid with urgency.

But as we wrote previously, DeFi ‘banks’ are just pieces of software connecting borrowers and lenders. They don’t have any capital reserves, so how can they ensure the stability of the lending system, should things go bad?

Liquidators

Luckily for us, crypto operates on the basis of having the right incentives in place.

In the ‘normal’ world, a bank would sell a bad loan to a debt collector at a discount or would liquidate the client’s position automatically if the collateral is liquid (i.e. margin call). Sometimes banks / brokers do it smoothly and sometimes they suffer losses.

In DeFi, the ‘liquidation’ function is outsourced to external capital providers who are incentivised (by money of course) to step in and repay someone’s bad debt. This happens automatically in a programmatic manner:

Having external capital providers on stand by ensure safety and stability of the lending protocols, while generating some nice IRRs for the liquidators. Such a system has been in place for a while now and so far it has been able to withstand substantial market corrections and credit events. In fact, it’s a normal part of a daily life of every lending protocol:

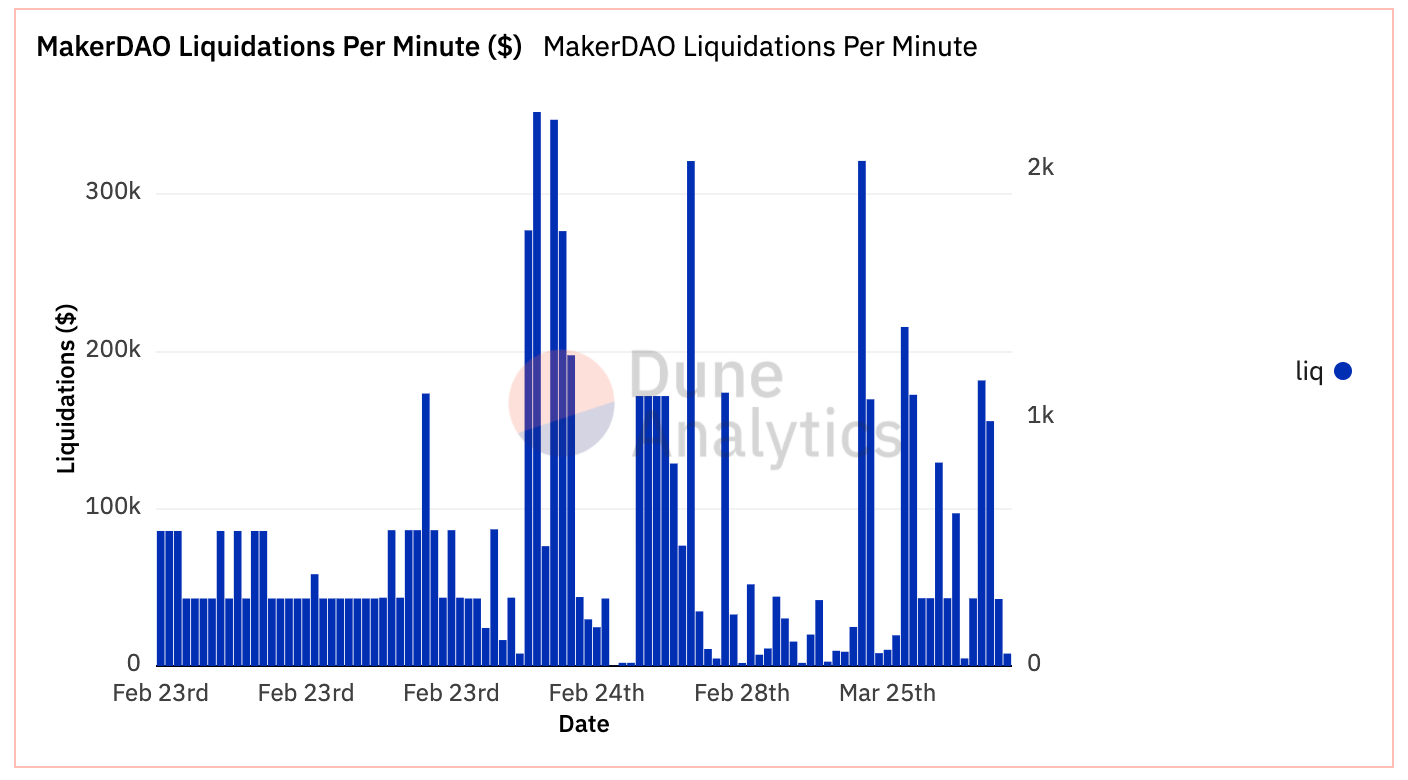

The image above shows Maker DAO - one of the oldest lending protocols - experiencing an average of $43k of liquidations per minute. All of this happens in the normal course of business without the protocol suffering any stress.

It’s a highly competitive business where debt liquidations happen in the matter of seconds and sophisticated bots are fighting to win the ‘bid’ for a specific margin call. Within a short timeframe this became a highly complex financial specialisation which requires very advance software fine-tuning to ensure the liquidator bot generates profits.

Liquidators - the silent lending market participants - are the reason why DeFi lending protocols are able to exist as software businesses without carrying their own capital or holding reserves. This innovation of spreading risks and incentives in a peer-to-peer manner is yet another example of crypto market ingenuity, paving the way for new business models.