Stay informed about what matters in crypto. Forget the noise. Get free market-leading crypto research by subscribing to Re7 Capital’s research below:

About Re7 Capital

Re7 Capital is a research-driven digital asset investment firm specialising in DeFi yield and liquid alpha strategies.

We’re Hiring!

Re7 is searching for an Investment Analyst and a DeFi Research Analyst!

If you are insanely passionate about crypto; if you can’t imagine NOT playing with every new Web3 platform that pops up; if in the last year you spent more time in web3 than outside - then we want to hear from you!

Apply here!

Summary

In this edition, we cover:

The 3 core layers of the liquid LSDFi market

Analysing products at the yield access layer

Pendle and Gearbox’s recent PMF and growth opportunities

Liquid Staking Derivative Finance (LSDFi)

With the prospect of interest rate cuts and lower treasury yields in 2024 and beyond, there is a higher risk premium in markets.

This comes at a time when new staking primitives (liquid re-staking) have come online within Web3, providing plenty of yield opportunities competing for capital.

Eiganlayer offers staking yields beyond vanilla ETH by enabling shared security models for a broad set of services on Ethereum.

The re-staking market is measured in billions of dollars.

These new staking primitives (e.g. Eigenlayer) have, in turn, driven the advent of other primitives that can optimise how investors capture those yields.

At a basic level, you can think of the stack in 3 parts:

Re-staking (foundational infrastructure allowing for Ethereum re-staking)

Asset (allows users to stake ETH and receive liquid re-staking tokens)

Yield access (infrastructure enabling investors to manage risk related to re-staking yield).

Digging Into the Yield Access Layer

On the one hand, you have Pendle Finance which allows the trading of future yield through tokenisation.

The vast majority of Pendle’s TVL today is driven by LRT yield speculation/trading.

On the other hand, you have infrastructure like Gearbox which provides a credit layer for users to borrow and lever up on their yield strategies.

Gearbox’s V3 upgrade brought credit accounts centred around smart contracts that manage collateral and borrowed funds.

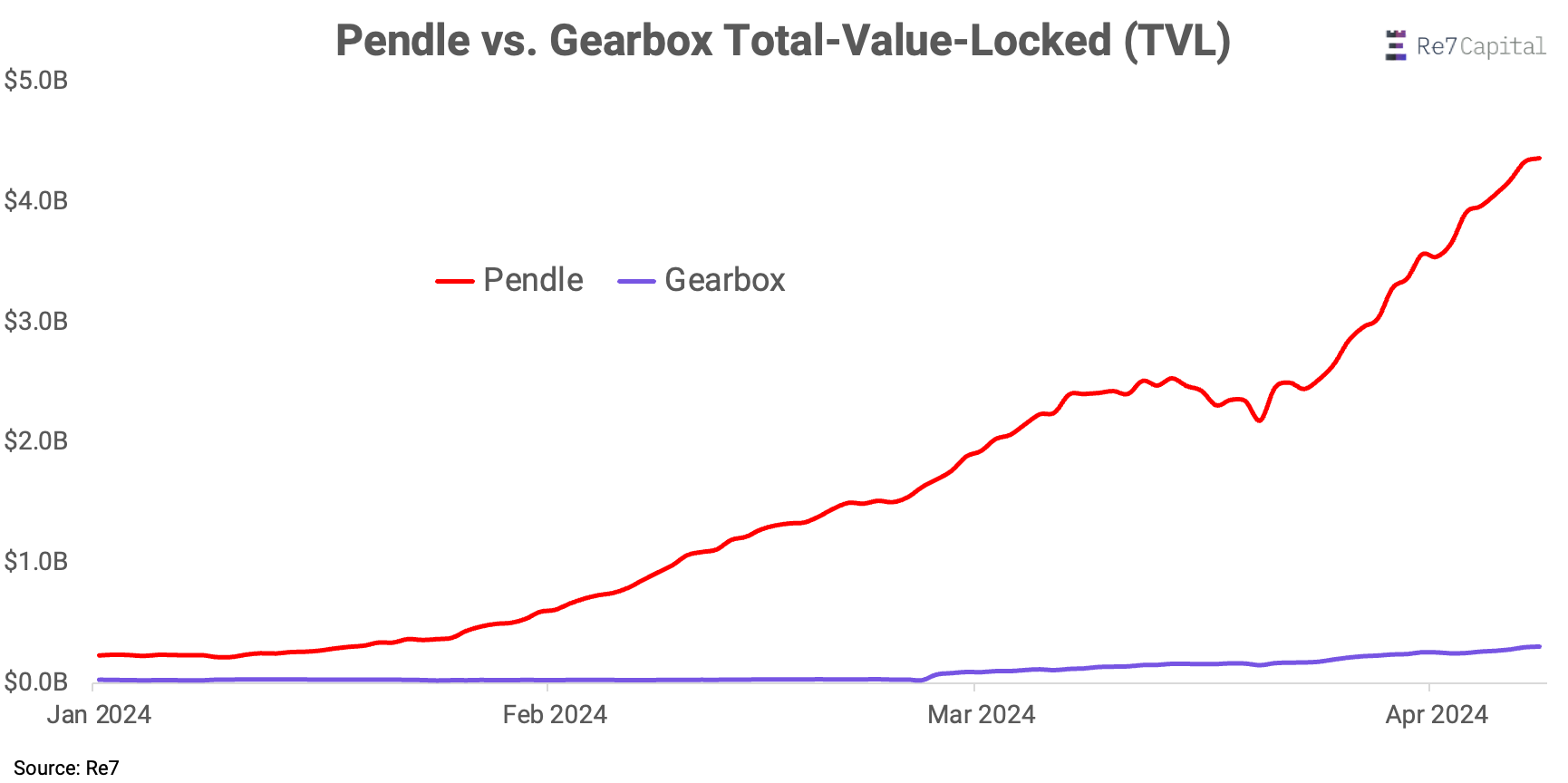

Zooming out, Pendle leads the pack for total value deposited value (TVL), breaching $4.3B vs. Gearbox’s $316m - a 13x difference.

That said, Re7 has been monitoring trends with the smaller player that are worth highlighting.

While lower in TVL, Gearbox’s total-value-locked has crossed $300m for the first time since V3 went live showing clear demand for ETH and stablecoin holders seeking 25%+ APY opportunities.

Gearbox’s active borrowers have breached 1k with growth being driven by an increasingly wider user base - not just the same account holders.

Arguably, better KPIs for protocols like Gearbox relate to demand/supply dynamics.

Gearbox’s lending capital has grown from $26m to over $250m in 60 days.

This has been met with higher demand with borrows crossing $220m - a new ATH level.

Having higher demand to supply has meant Gearbox has grown at an accelerated rate while also maintaining ATH in supply rates. Utilisation rates across main pools have kept relatively high >50-80%.

Gearbox’s strong PMF since launching V3 has translated to ATH in revenue forecasts.

Revenue for leverage protocols like Gearbox is accrued over the ‘loan’ period but paid at closure.

Using a simple formula, we can project Gearbox revenue for each pool on an annualised basis:

Pool revenue = (expected liquidity - total borrowed - available liquidity) * fee interest

Note revenue projections can be fluid based on several variables, including the number of pools supported in Gearbox.

Across its 6 pools, Gearbox is currently projected to generate over $17m in annualised revenue which is shared with GEAR stakers.

Coming full circle, our analysis shows Gearbox is potentially generating higher revenue relative to TVL vs. Pendle.

This may be an early signal that credit infrastructure like Gearbox may be more efficient at capturing value than tokenised yield infrastructure today.

Of course, this may change with product and re-staking infrastructure development.

The liquid re-staking market is complex but still nascent market with more LRT products coming to market seemingly every week for investors.

Both Pendle and Gearbox stand to benefit from this market growth in their unique ways as both look to expand further into the market.

What will be even more interesting is how both platforms could integrate one another in a true mutualistic fashion.

What’s more clear is teams are laser-focused on growing the pie.

Then deciding how to eat it.

Aptos

Last week, Re7 analysed the Aptos ecosystem as part of OurNetwork’s first deep Zoom-in series.

Here’s a taster of the signals we picked up:

Aptos Daily DEX Volume Passes $40M with New Features

Cellana is a new ve(3,3) DEX. Airdrops to early Aptos users and a strong emissions program have pushed the DEX’s TVL to over $30M in the span of a few weeks.

The first month of trading fees exceeded $500k annualized, all passed back to veCELL token stakers.

Much of the volume on Aptos DEXs comes from larger pairs and cross-chain txs such as APT, WETH, WBTC, USDC/USDT, with additional volume coming from meme coins and newly launched DeFi ecosystem tokens.

What does this mean looking ahead? With activity and volume picking up, the CELL ve(3,3) model will likely continue to generate high fees which are distributed to veCELL holders on a pro-rata basis

Global MCAP

$2.6T; Global market capitalisation continues to consolidate around $2.5T in the past week.

ETH/BTC

0.0503; ETH/BTC still fighting its long-term support level of 0.05 as BTC sees relative strength heading into its halvening (est. 18th April 2024).

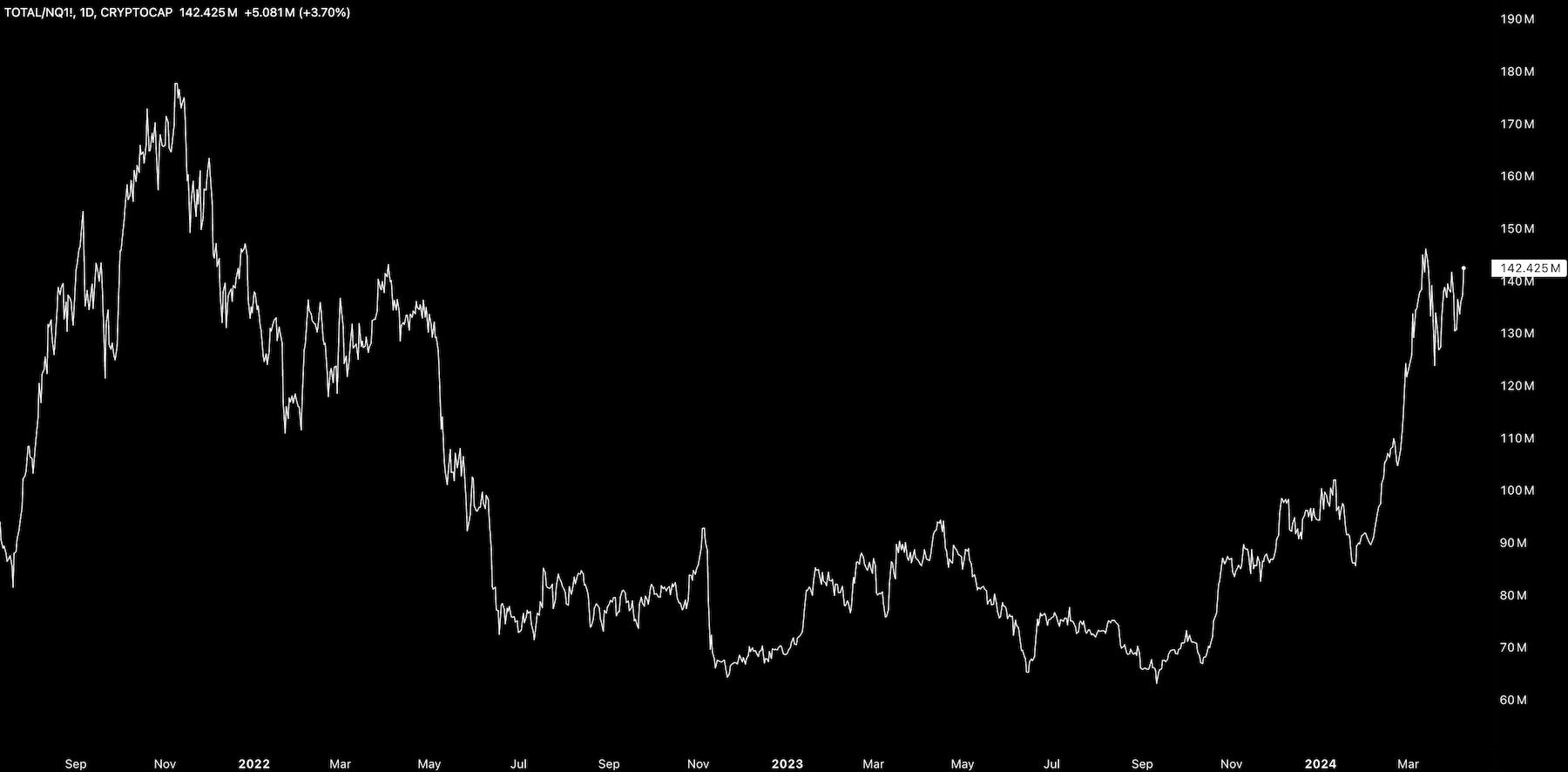

Crypto/Nasdaq Fut

Crypto is looking to break out against NDX and make new yearly highs. Crypto has been outperforming the index since September 2023 by 125%.

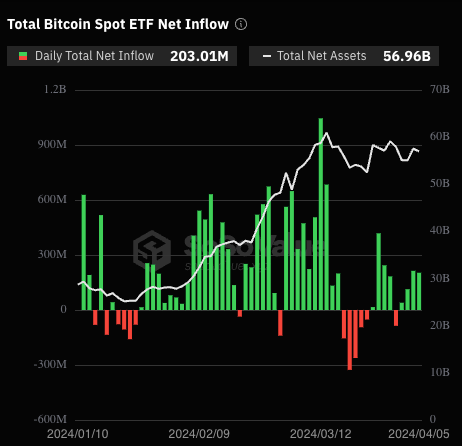

Bitcoin ETF Net Inflows

$200m+; US Bitcoin spot ETFs are seeing net inflows. Cumulative total net inflows have climbed to $12.61B.

ICYMI: Re7’s Latest Contribution to OurNetwork

Disclaimers

The content is for informational purposes. None of the content is meant to be investment advice. Use your own discretion and independent decision regarding investments. The opinions expressed in all Re7 public research articles are the independent opinions of the authors at the time of publication and not the opinions of the affiliates of Re7.

Please see here for full disclaimers.