The Old Fashioned recipe

We’ve come a long way since 1602 when Amsterdam Stock Exchange - the world’s first formal stock exchange - was founded by the Dutch East India Company.

While the process of trading has shifted from ‘outcry’ auctions to high frequency algorithms, the actual logic and business model have stayed the same. Professional market participants quote prices at which they are willing to buy and sell assets and collect a bid-ask spread for the service of providing liquidity (market making).

These services are provided on centralised venues, called exchanges. Exchanges are centralised locations where trading can occur and their utility comes from pooling all market liquidity in one place and lowering trading friction. Naturally, this comes at a price.

It’s a fair business model - financial intermediaries provide ‘price discovery’ services, helping retail and institutional investors get the best price available in the market at a particular moment in time. In exchange they capture certain economic value from that transactional flow.

The world is changing, however, and as we are evolving from centralised to distributed networks, we have to ask ourselves - are these intermediaries still needed? And even if they are, should they be capturing so much value for themselves or should it be distributed differently?

Before crypto networks arrived, these were political and philosophical questions. Now it’s a question of technology and business models. Actually, it’s not even a question anymore.

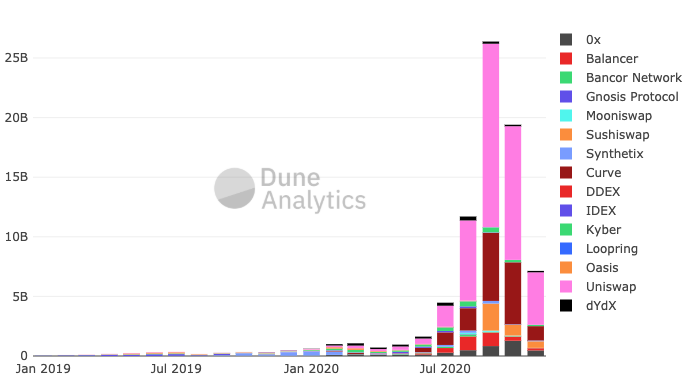

Distributed networks are already here with $74bn traded via ‘decentralised exchanges’ (DEXs) in the last year and the number is growing.

What’s a DEX and why should we care?

These are pieces of code, also referred to as Automated Market Makers (AMM), and their mission is to quote prices between two assets according to a simple pricing algorithm.

The contract checks if your wallet has sufficient funds and tells you the exchange rate you are going to get if you place the order - that’s it! The function of an exchange / broker is fulfilled by an open-sourced piece of code deployed by a team of ~10 people. This year there have already been instances when this specific DEX (Uniswap) processed more trading volume than Coinbase - one of the largest traditional crypto brokers with 1123 employees.

While this has obvious implications for the profitability of such businesses, this is just the tip of the iceberg. As we previously noted, the main value any trading platform provides is liquidity. In the traditional world we are used to screens like this:

While most investors typically place their buy and sell orders and patiently await execution, most trading volume is flowing through market makers - High Frequency Trading firms - they place their orders in microseconds, ensure the market stays liquid and earn their profit spread. These are professional institutional players extracting economic rent from trading.

Crypto, however, as we already know is all about ‘ownership economy’ and value redistribution to its users. So in this market, instead of relying on professional funds, Automated Market Makers allow their users to place their savings into so-called liquidity pools and earn profits on them. Simply put, any user can place funds into this smart contract and a DEX will perform ‘market making’ on their behalf and distribute profits to its users.

Every time a trade goes through, liquidity providers to AMMs earn fees on the assets they provide. They are effectively replacing professional participants with value flowing into the ‘community’. Not only that, the protocols also allocate their own coins to such users, further increasing loyalty, traction and liquidity - a virtuous loop.

Individual investors are now capturing economic value previously only available to institutional investors; they have more power over how they can deploy their savings and all of this is done at a fraction of the costs of traditional solutions. Strong growth and increasing market share of DEXs took place despite complex user interface and what is generally quite a tedious process. This is how old businesses get disrupted.

By the way, this disruption is quite a profitable one.

It’s not about crypto

Let’s go back to stablecoins for a second. As we know, these are coins linked to a particular underlying asset with a 1:1 ratio. We’ve looked at USD, but why stop there? Why not oil, gold or stocks?

‘Real’ assets are already being traded on such platforms via their crypto alter-egos. Crypto plays its role here not in the context of cryptocurrencies, but as technological ‘rails’ upon which transactions can flow, even real world transactions. And that’s why DEXs matter.