Stay informed about what matters in crypto. Forget the noise. Get free market-leading crypto research by subscribing to Re7 Capital’s research below:

About Re7 Capital

Re7 Capital is a research-driven digital asset investment firm specialising in DeFi yield and liquid alpha strategies.

We’re Hiring!

Re7 is searching for an Investment Analyst and a DeFi Research Analyst!

If you are insanely passionate about crypto; if you can’t imagine NOT playing with every new Web3 platform that pops up; if in the last year you spent more time in web3 than outside - then we want to hear from you!

Apply here!

Summary

In this edition, we cover:

Re7’s macro framework highlights

The intersection between macro and crypto:

How the business and liquidity cycle drives crypto

Informing crypto performance vs. NASDAQ

Informing altcoin dominance within crypto

Informing Re7’s asset lag theory and why NFTs are the last class to react in a cycle

The Macroeconomic Setup

We live in a debt-based world economy.

With central banks running with increased deficits, due to stimulating the economy and stamping out inflation, interest payments due on their debt have equally surged.

Take the largest and most important economy to consider here - the US.

US national debt interest payment is expected to total $870B in the 2024 fiscal year.

Entering a Period of Balance Sheet Expansion

The Fed faces two choices: it either has to face record debts leading to a dislocated bond market or they have to expand its balance sheet to service the debt.

With the first option out of the question, the only available option left is to expand the balance sheet, providing an accommodating (not restrictive) environment for risk assets.

The need for balance sheet expansion is also driven by the slowdown in economic growth from rate hikes.

The business cycle leads the liquidity cycle which, in turn, drives risk asset performance.

Entering a Period of Global Liquidity Expansion

The global economy is rebounding in a typical cyclical fashion. The ISM, a key indicator of the state of the US economy, bottomed as higher interest rates took hold of economic activity.

Now the ISM is reversing and we are entering a growth phase.

And it isn’t just a US story but a global story…

This growth phase is typically coupled with liquidity expansion as central banks service their debt and also support the economy following periods of economic slowdowns.

In effect, liquidity always tries to play ‘catch up’.

This is why the US economy typically leads trends in global liquidity by ~15 months

Its lead further supports we are in the early phases of a liquidity expansion period.

And when it comes to inflation, lagging components like real estate, that drive the indices, are continuing to trend down.

Central banks have every incentive to overshoot inflation to provide themselves a reason to lower interest rates to ease the debt interest payment burden.

With inflation remaining sticky above the Fed’s current 2% target, we’ve still seen ATHs in risk asset indices like NASDAQ and BTC in Q1 2024.

With markets being forward-looking, they have largely shrugged off inflation concerns as they effectively see monetary expansion as the inevitable path until mid-2025.

Where Crypto Fits in With All of This

Just like all other risk assets, crypto prices move in line with liquidity.

As liquidity expands due to the business cycle, cryptoasset prices have rallied…

During times of liquidity expansions (i.e. bull markets), riskier assets have historically outperformed as investors rotate their capital down the risk continuum.

Take the BTC/NASDAQ 100 ratio.

BTC/NDX has now broken above its cycle ‘wedge’ akin to Q3-Q4 2020 as the market starts pricing in accelerated liquidity expansion.

Macro and the Altcoin Market

We can also use the liquidity expansion to colour Re7’s two-phase bull market framework.

Phase 1: Global crypto market rallies off its bear cycle bottom while the Altcoin dominance remains flat/declines

Phase 2: Altcoin dominance turns positive as bull market momentum strengthens

Historically, layering into liquid alpha during Phase 1 has been the opportunistic window despite beta remaining relatively strong in the market in this period.

We may have already entered Phase 1 of the bull market but we have yet to see the logarithmic growth seen in early 2021.

As liquidity expansion gets underway (and rate cuts ensue), altcoin dominance surges.

This occurred soon after BTC broke its ATH convincingly in December 2020 with BTC typically leading the market during Phase 1.

Macro and NFTs

And within the altcoin market, we can identify the riskier portion of the market such as NFTs.

Re7’s Asset Lag theory states the more speculative assets are the last to react in any liquidity cycle - typically 12-15 months in any given economy.

Second-hand watches (an example speculative asset) are only just bottoming out.

This is due to what’s known as the ‘wealth effect’ - the behavioural economic theory that consumers spend more when their wealth increases even if their income does not.

The blue-chip NFT collection CryptoPunks seems to have formed a price bottom (ETH) 12-15m after ETH/USD bottomed in June 2022.

Coming full circle, central banks having to bias toward liquidity expansion (vs. restriction) means the heightened speculation already found in memecoins today is coherent…

So to conclude, the early innings of the current bull market reflect the early stages of liquidity expansion and growth period.

As more capital flows into crypto reach record levels, more capital can be put to work within an increasing number of Web3 protocols and applications.

What’s more? Increased capital, in turn, can drive measurable value back to those respective protocols and applications.

Do All Roads Lead to Ethena?

The cash and carry trade is alive and well with Ethena's structured product "stablecoin" which earns yield by holding staked ETH spot tokens and shorting perpetual on various exchanges.

In the up-only price environment, this trade has been lucrative, netting an average of over 45% annualized yield for USDe stakers.

The result is that many other protocols have looked to integrate the Ethena product as a yield source.

Most notable is MakerDAO, which has an executive vote in progress to acquire sUSDe through a custodian and eventually integrate it to provide cheap DAI debt to borrowers using sUSDe collateral.

Re7 Labs is also enabling a similar trade with our Re7USDT MetaMorpho vault that will launch this week.

An initial 10m supply cap is set for the sUSDe market, allowing supplying users to deposit USDT for yield and sUSDe holders to borrow USDT against their collateral for over 10x leverage.

The expectation is that with funding rates continuing to stay high it represents a strong opportunity for leveraged yield. With caps of 10m to start, we expect the demand for both sides of the market to be high, so be ready to ape when the vault goes live later in the week.

Global MCAP

$2.5T; Global market capitalisation faces resistance at the $2.5T mark - just 18% below ATH levels. Crypto market has yet to enter true price discovery.

ETH/BTC

0.05258; ETH/BTC still kept within its multi-year wedge, being pulled down to resistance yet again due to relatively strong BTC performance/flows from US ETFs. 0.05 likely to prove strong support yet again.

SOL/ETH

SOL/ETH performed a decisive break above its ascending wedge as highlighted last week.

Global Spot Exchange Volume

$90B; Daily exchange volume still near 10x from the bottom, similar volume levels to Q3-Q4 2021 but still 30% below ATHs.

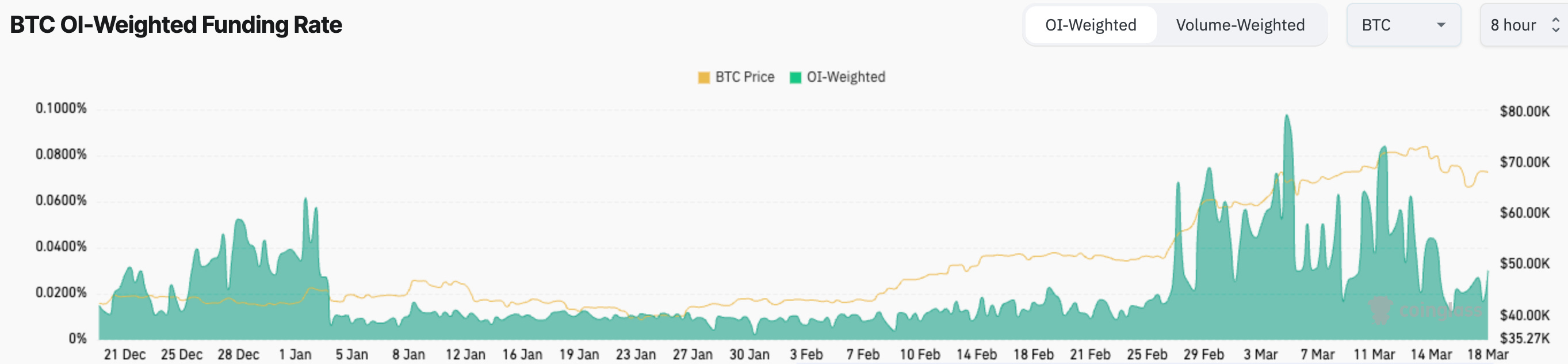

Futures

OI-weighted funding rates remain elevated at +0.032% as traders ease on the bullish positioning. OI remains just below ATH $35B.

ICYMI: Re7’s Latest Contribution to OurNetwork

Disclaimers

The content is for informational purposes. None of the content is meant to be investment advice. Use your own discretion and independent decision regarding investments. The opinions expressed in all Re7 public research articles are the independent opinions of the authors at the time of publication and not the opinions of the affiliates of Re7.

Please see here for full disclaimers.